The Business Case

For NxGen Liability Management &

Financial Professional Program

For NxGen Liability Management &

Financial Professional Program

|

The Underserved, debt burdened milleniel & mass-affluent market looking for solution to

|

Pain Point For Investors

|

|

|

|

Disconnect of Financial Professionals

|

Pain Point For Financial Professionals

|

The NxGen Program Solution that builds trust, knowledge and anexecutable planning process for wealth building

NxGen Family Office Fills The Gap

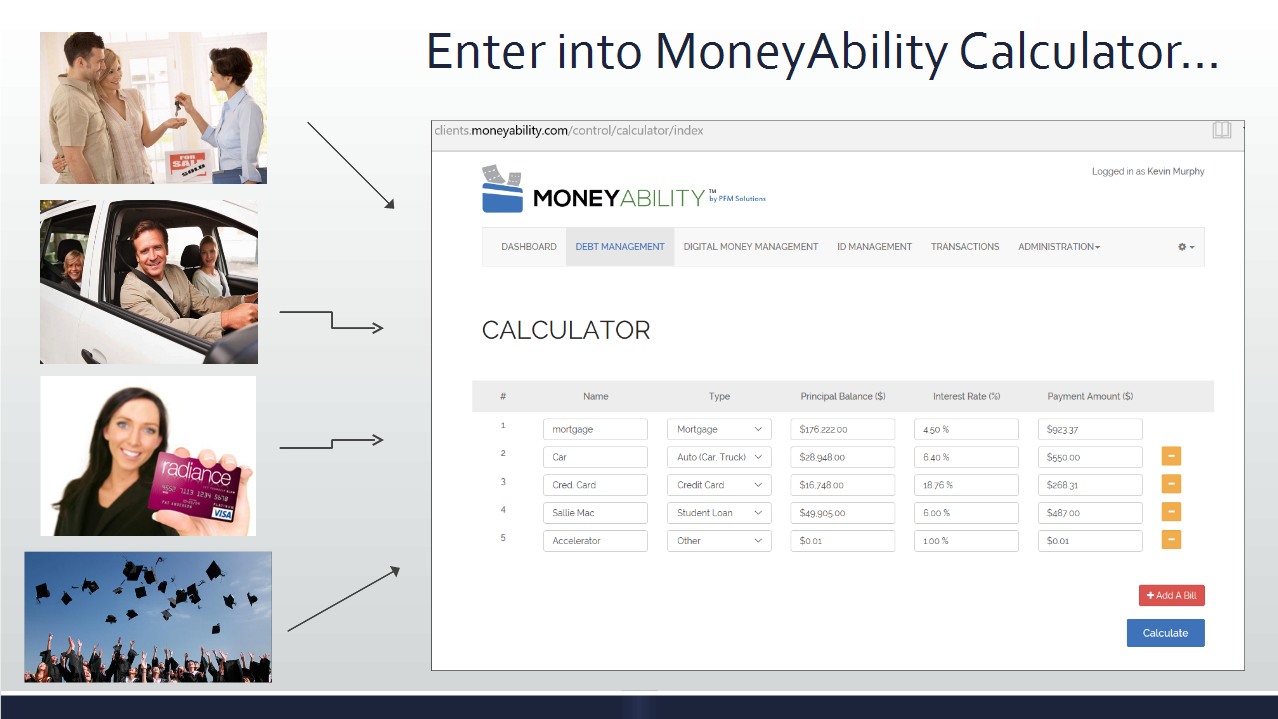

How It Works

|

|

|

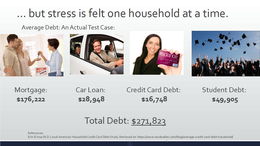

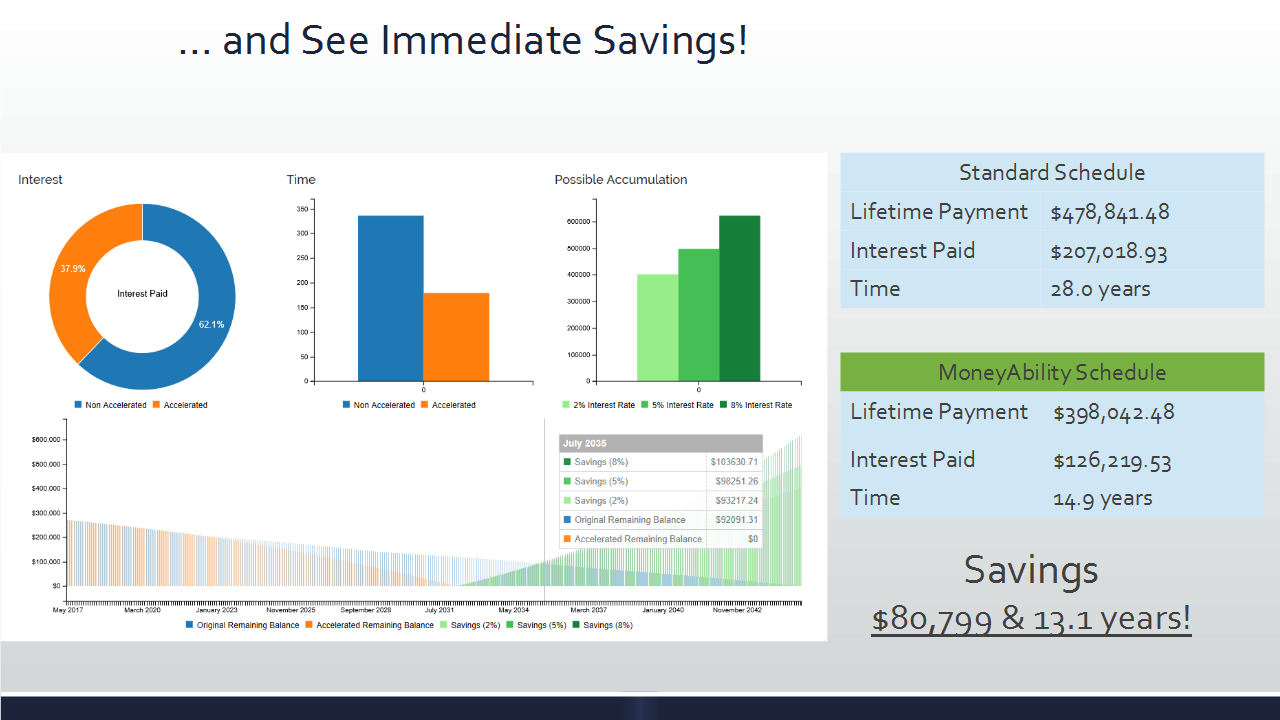

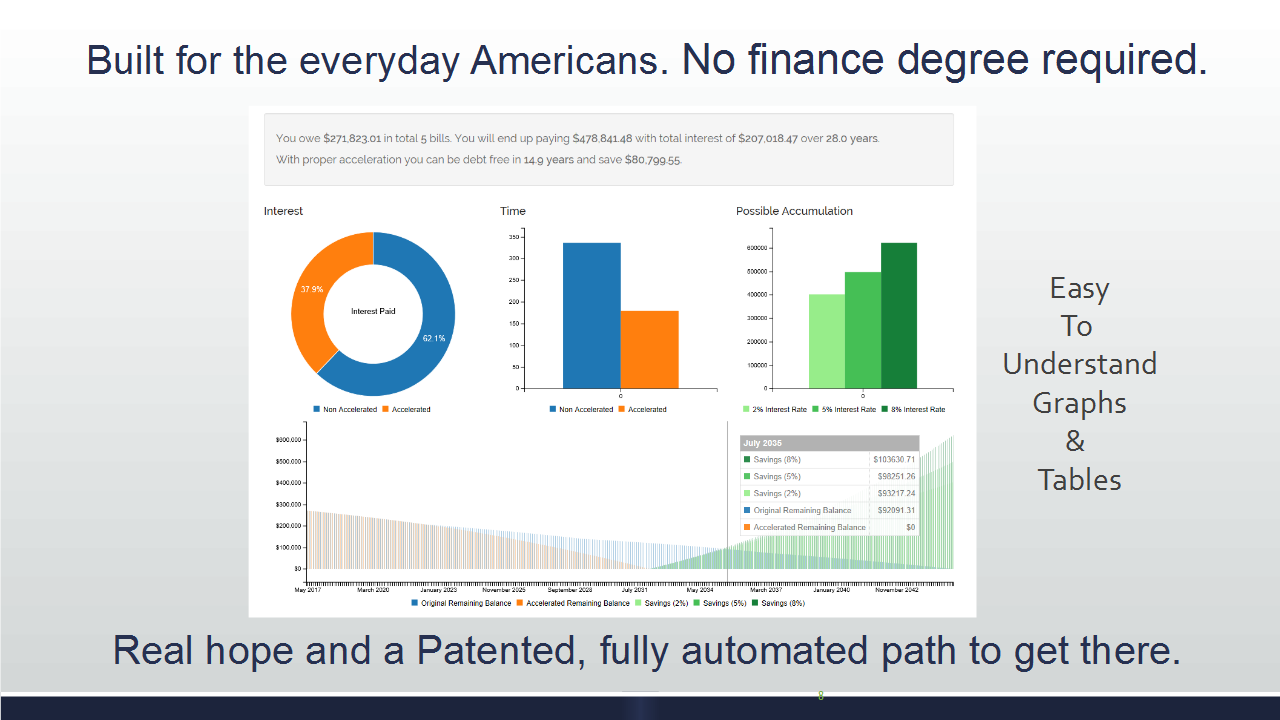

Automated & Comprehensive Financial Program

Personal Financial Management System

- Debt Management

- Digital Money Management

- ID Management

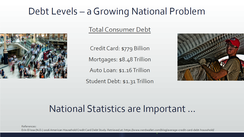

Statistics

- At 75 million, Millennials represent the largest living generation in the United States. The vast majority of them do not have a financial advisor or even invest money.

- In fact, 79% of Americans aged 18 to 34 do not invest.

- That figure rises even higher to 85% for millennial women.

- Millennials have higher levels of student loan debt, poverty and unemployment, combined with lower levels of wealth and personal income than their predecessor generations did in the same stage of life.

- Despite the bleak statistic, they are not lacking in resources to invest altogether. Millennials are the best-educated cohort to date, which is highly correlated to economic success. They are also on track to receive the greatest wealth transfer in history from their Baby Boomer parents. PwC estimates that by 2020 Millennials and Gen Xers will control more than half of all investable assets, or about $30 trillion.

- Too confusing: 69% find investing to be overly complex

- Unrelatable: 60% of millennial women equate a typical investor to an old, white male

- Tech dependence: Over one third say they would trust an app with their money more than traditional investment firms

- Not enough money: 41% believe they don’t have sufficient funds to invest

- Compared to the general population, LGBT clients feel much less prepared to make wise financial decisions and lack basic knowledge regarding money management, according to a 2016-17 study conducted by Prudential Financial.

- This is especially true for the younger cohort: 6 in 10 LGBT millennial and Gen X respondents said they are uncomfortable knowing what, when or where to buy and sell.

- The study shows that LGBT clients make on average more than the general population (25% of households make over $100,000 a year) and have comparable levels of debt, with close to half holding less than $10,000.

- Only a third of LBGT clients employ a financial advisor, which means there is significant room for growth in this market for planners who are willing to make the effort to understand the unique needs and challenges of this community.

ADVISORS

- 70% of top financial advisors (those who earn $1 million or more annually) focus on niche clients or a specific component of the advisory market. Many go further to concentrate on a niche within a niche.

If advisors can dispel some of those stereotypes and learn to speak the language of Millennials, the opportunities to build a niche business are endless.

- There are over 26.3 million foreigners working in the United States, and millions more who are living here in various situations. Moving to a new country is a daunting enough challenge, making financial decisions even more so.

How do I file my taxes? How do I purchase a home? Can I take out a loan from the bank? Can I start a small business? I’m not American, can I still save for retirement here? What happens when I decide to go home? These are all important questions foreign nationals must address, and the consequences for getting them wrong can be serious.

This is where financial advisors can step in to help. There is significant room for specialization here, such as highly-skilled workers on H1B/O-1 visas, or people from specific regions like Europe or Asia. It will take some time to learn the specific requirements and laws your niche has to meet, but the rewards will be plentiful if you can establish yourself as the expert.

In Short: Building your entire practice on one type of client is no easy task. There is a considerable amount of extra information and vernacular to learn; it also takes more than just time and education to gain the trust of a community you may not have any relationships with. But that is exactly why these clients are underserved and in great need of professional assistance.

Introduction: Council of Economic Advisors

Introduction Millennials, the cohort of Americans born between 1980 and the mid-2000s, are the largest generation in the U.S., representing one-third of the total U.S. population in 2013. 1 With the first cohort of Millennials only in their early thirties, most members of this generation are at the beginning of their careers and so will be an important engine of the economy in the decades to come. The significance of Millennials extends beyond their numbers. This is the first generation to have had access to the Internet during their formative years. Millennials also stand out because they are the most diverse and educated generation to date: 42 percent identify with a race or ethnicity other than non-Hispanic white, around twice the share of the Baby Boomer generation when they were the same age.2 About 61 percent of adult Millennials have attended college, whereas only 46 percent of the Baby Boomers did so. 3 Yet perhaps the most important marker for Millennials is that many of them have come of age during a very difficult time in our economy, as the oldest Millennials were just 27 years old when the recession began in December 2007. As unemployment surged from 2007 to 2009, many Millennials struggled to find a hold in the labor market. They made important decisions about their educational and career paths, including whether and where to attend college, during a time of great economic uncertainty. Their early adult lives have been shaped by the experience of establishing their careers at a time when economic opportunities are relatively scarce. Today, although the economy is well into its recovery, the recession still affects lives of Millennials and will likely continue to do so for years to come. This report takes an early look at this generation’s adult lives so far, including how they are faring in the labor market and how they are organizing their personal lives. This generation is marked by transformations at nearly every important milestone: from changes in parenting practices and schooling choices, to the condition of the U.S. economy they entered, to their own choices about home and family. However, in many cases, Millennials are simply following the patterns of change that began generations ago. Millennials are also the generation that will shape our economy for decades to come, and no one understands that more that the President. It’s why he has put in place policies to address the various challenges their generation faces. This includes policies such as: making student loan payments more affordable; promoting digital literacy and innovation; pushing for equal pay and paycheck fairness; supporting investments and policies that create better-paying jobs; connecting more Americans to job training and skills programs that prepare them for in-demand jobs; supporting access to credit for those who want to buy a home; and increasing access to affordable health care. And it’s why the 1 Census Bureau. There is no strong consensus about how to define Millennials, though several sources attribute the word to historians Neil Howe and William Strauss, who outlined a theory of social generations in American history. 2 Decennial Census and American Community Survey. Data for Millennials are for those 15 to 34 years old in 2012. Baby Boomers comparisons are for when they were 15 to 34 as surveyed in 1980. 3 Decennial Census and American Community Survey. Data for Millennials are for those 18 to 34 years old in 2012. Baby Boomers comparisons are for when they were 18 to 34 as surveyed in 1980. 4 President will continue to act with Congress and on his own where he can to build on this progress to expand opportunity for Millennials and all Americans.

Conslusion

So, while there are substantial challenges to meet, no generation has been better equipped to overcome them than Millennials. They are skilled with technology, determined, diverse, and more educated than any previous generation. Millennials are still in the early stages of joining and participating in the labor market. Taking steps to help them access and complete college, manage their student debt, have better opportunities for training and connection to jobs, access the credit they need for a home, protect the network neutrality that is the basis for much of their technological activity, as well as general policies to strengthen investment, job creation and wage growth, all have the potential to have a lasting impact for this generation and thus for U.S. economic performance for decades to come.